Strategy’s $BTC Reserve: What’s the End-Game?

Bitcoin’s price has been a rollercoaster, peaking at $110,000 in late 2024 before sliding into a downtrend, now hovering around $84,000 as of March 31, 2025. Yet, this dip hasn’t deterred Strategy—formerly known as MicroStrategy—from doubling down on its Bitcoin bet. The company has amassed a staggering 528,000+ BTC, positioning itself as the largest corporate holder of Bitcoin in the world. This accounts for roughly >2.5% of Bitcoin’s total supply, a figure that underscores Strategy’s unrelenting commitment to the cryptocurrency. But what’s the end-game here?

The Acquisition Machine

The Bitcoin buying spree began in 2020 when Strategy transitioned $250 million cash reserves into Bitcoin. Since then, the company has aggressively raised funds by selling shares, raising billions in 2024 alone. Strategy has also tapped creative debt tools, including convertible senior notes and perpetual strife preferred stock, designed specifically to fund Bitcoin acquisitions without tying up existing holdings. Strategy is never exhausted of innovative financing to raise capital.

In every market condition, Strategy maintained its clear vision and continued accumulating, adding to its reserves. The buying spree was especially aggressive during the 2024 bull run—will it pay off?

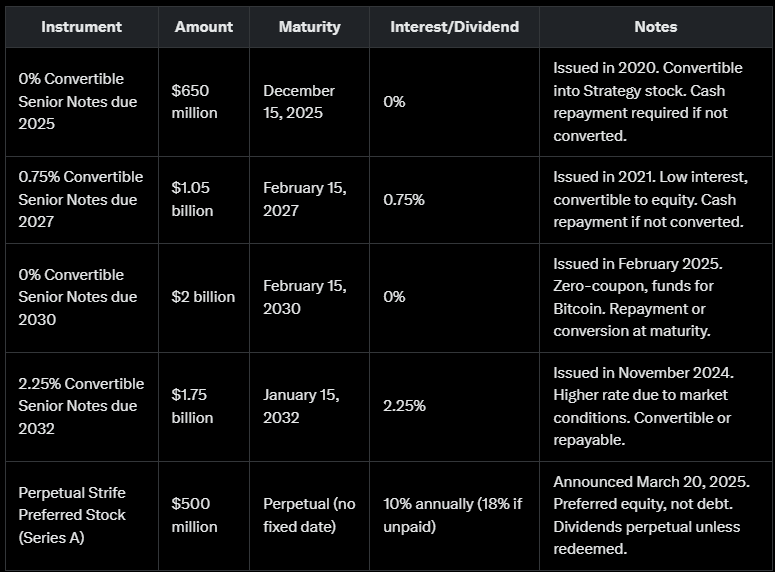

The Debt Story

As of late 2024, Strategy’s total liabilities are around $4.57 billion, majorly tied to convertible notes. With an additional $2 billion from 2030 notes and $500 million from preferred stock issued in 2025, the company’s total debt burden is well over $7 billion. These obligations carry specific maturity dates, at which point Strategy must either repay the principal or convert the debt into equity.

Here’s a breakdown of the key debt instruments and their due dates:

When Does Strategy “Owe”?

- Short-Term (2025): The $650 million due December 15, 2025, is the first major test. With over $33 billion spent on Bitcoin and a market cap exceeding $50 billion. if the stock price is below the conversion price, Strategy must repay the maturity amount.

- Mid-Term (2027-2032): Larger repayments ($1.05 billion in 2027, $2 billion in 2030, $1.75 billion in 2032) loom, but the long timeline gives flexibility.

- Ongoing: The 10% preferred stock dividends (~$50 million annually) start in 2025 and continue indefinitely unless redeemed.

Strategy’s debt is unsecured, no immediate liquidation risk tied to Bitcoin’s price (unlike margin loans). Michael Saylor’s strategy assumes Bitcoin’s long-term appreciation will outpace debt costs, avoiding the need to sell BTC. Posts on X and company statements suggest no repayment pressure unless Bitcoin plummets and stays low, forcing cash raises at unfavorable terms.

Although Strategy does not owe MSTR equity investors direct payments, they are affected by how the company manages its debts. In the worst-case scenario, if $BTC tanks and Strategy cannot service its maturing debts, it might issue more shares, diluting shareholders.

Liquidation Risk

Liquidation risk at present context refers to the possibility that Strategy would be forced to sell its Bitcoin reserve — currently 528,000+ BTC — to meet financial obligations or avoid insolvency.

First Major Repayment Convertible at approximately $121.01 per share (adjusted). If unconverted, cash repayment is required. Strategy’s substantial profit and loss (PnL) on its Bitcoin reserve should be sufficient to cover it.

Hefty debt repayments from 2027 to 2032 remain uncertain, as longer-term repayments are closely tied to MSTR’s share price and BTC’s price. If unconverted at maturity, Strategy will be forced to liquidate portions of its reserves for cash repayments. The longer-term maturity timeline offers some hope that Bitcoin will follow an upward trajectory.

The minimal interest and longer-term convertible notes pose less risk compared to the Perpetual Strife Preferred Stock, where Strategy is liable to pay a 10% annual dividend on $500 million. Non-payment increases the rate to 18%.

Liquidation Risk Scenarios

Liquidation risk scenario for upcoming december debt repayment. As of Today (March 31, 2025), Strategy’s Bitcoin reserve faces low liquidation risk.

End-Game

Strategy (formerly MicroStrategy) was highly efficient in raising capital through various debt instruments and acquiring a significant portion of Bitcoin’s supply. Michael Saylor’s sole thesis for going all-in rests on the hope that Bitcoin will maintain a perpetual upward trajectory. Looking back, Bitcoin has indeed followed an upward trend.

Starting in 2027, larger debt repayments, combined with perpetual dividends, will put pressure on Saylor. The assumption of a continuously rising Bitcoin price may not always hold true.

Bitcoin is just another risk asset, partially correlated with equities. The narrative of it being “digital gold” has never gained traction, and it is not a safe-haven asset like gold. Risk assets tend to plummet during uncertainties, such as recessions, and Bitcoin has yet to experience a recession. If and when Bitcoin drops below $25,000—a 70% decline from current levels—Strategy could find itself out of strategy. Given Bitcoin’s history, a 70% drop is plausible.

Saylor’s confidence in never selling Bitcoin is a massive bet. It’s a make-it-or-break-it gamble with no middle ground.

Leave a comment